KARACHI: Industry leaders were taken by surprise when the State Bank of Pakistan (SBP) announced a sharp cut of two percentage points in the key policy rate after an emergency meeting of the Monetary Policy Committee (MPC) on Thursday.

The rate cut has turned the clock back to the fall of 2018, when the newly arrived Pakistan Tehreek-i-Insaf government had just entered into talks for a large bailout package with the International Monetary Fund (IMF) and the key target policy rate was raised from 8.5 per cent to 10pc. For its part, the IMF had asked for a six percentage point hike in the rate as a prior condition for programme accession, according to then finance minister Asad Umar.

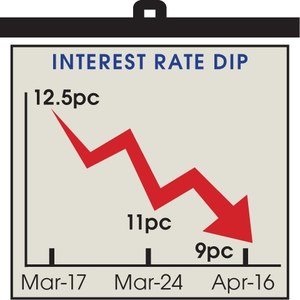

Thursday’s action took the policy rate down to 9pc, back in single digit territory for the first time since that fateful fall. It is the third rate cut in 30 days, and the second time that the State Bank has called an emergency meeting of the MPC in the past 30 days. By itself this makes the move historic since nobody can recall when in the last decade and a half at least, the policy rate was reduced so sharply and in so hurried a fashion.

Trigger for the decision was the projections contained in the World Economic Outlook report released by the IMF on Tuesday. The report said the world economy is set to contract by 3pc this year — “worst downturn since the Great Depression” — and Pakistan’s economy will see a contraction of 1.5pc in the ongoing fiscal year.

In a third cut in 30 days, policy rate comes down to 9pc

“Moreover, there are severe risks of a worse outcome,” the SBP said in a statement issued after the meeting. Meaning things are likely to get worse still.

This was an alarming projection. Pakistan’s economy has been seeing a growth rate of roughly 3pc in the quarters of the ongoing fiscal year thus far, so a net contraction by the end of the year would mean the fourth quarter, that runs from April to June, will see a contraction so sharp as to negate the effects of all three preceding quarters and push the growth of real output of the economy into negative territory. This was worse than what had been projected in the last emergency MPC meeting on March 24.

The State Bank, after acquiring further detailed data from the IMF on which the projection was based, and combining it with its own collection of high frequency indicators — “retail sales, credit card spending, cement production, export orders, tax collections, and mobility data from Google’s recently introduced Community Mobility Reports” as per the statement released after the meeting — ran its own models on the revised data to ascertain the depth of the contraction that the economy is about to register.

The results showed that growth would indeed be negative 1.5pc this fiscal year, while inflation is likely to descend to 9pc monthly average by June, where it was projected to be between 11pc and 12pc on March 24. For the next fiscal year, the State Bank’s projections showed inflation coming in between 7pc and 9pc by the end of the year.

Economists generally agree that interest rates should be at least equal, if not slightly above, the projected monthly inflation rate. Given the revised projections that the SBP was looking at in light of the new data, it was concluded that an immediate rate cut of 2pc was possible.

The projections were all run on Wednesday and by Thursday morning requests were sent out to all MPC members for an emergency meeting. According to various members who participated, the meeting lasted “a few hours” and ended somewhere around 5pm. The analysis that was shared with the meeting participants, who were assembled via digital platform, was that the State Bank is now seeing a collapsing growth rate, decline in inflation and a relative easing of the external situation, which creates the space and rationale for a possible rate cut.

“From here the decision was whether to wait for the scheduled MPC meeting in May, or move now,” says one participant. “Given the emergency times we are passing through, it was decided to move now.”

The IMF data was showing that the current account deficit will shrink from 5.0pc last year to 1.7pc this fiscal year, and come in closer to 2.4pc next year.

“Despite the growth challenges, the external position showed relative easing in the months ahead because of large multilateral inflows that are already scheduled, coupled with the debt relief under the G20 plan for which Pakistan has already qualified,” says the participant.

These are the wages of recession, falling inflation and external deficits. And this is what the State Bank reacted to on Thursday, for the second time in three weeks.